NOT FOR DISTRIBUTION TO U.S. NEWSWIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES.

The prospectus supplement, the corresponding base shelf prospectus and any amendment thereto in connection with the financing will be accessible through SEDAR+ within two business days

CALGARY, ALBERTA, (GLOBE NEWSWIRE – December 9, 2024) – Freehold Royalties Ltd. (Freehold or the Company) (TSX:FRU) has entered into a definitive agreement with a private seller to acquire mineral title and royalty interests in the core of the Midland Basin in Texas (the Acquisition or the Acquired Assets) for approximately $216 million, net of estimates for exchange rate and customary closing adjustments.

Acquisition Snapshot

- 1,250 – 1,350 boe/d of premium priced, light oil weighted production (~800 bbls/d oil)

- Approximately $31 million in 2025E net royalty revenue (net of production and ad valorem taxes and assuming US$70/bbl WTI)

- ~244,000 gross drilling acres, expanding our core, resource rich Midland Basin footprint by ~35%

- Highly undeveloped asset with ~25% of lands not having any horizontal drilling activity to date

- ~95% of production operated by Midland Basin focused ExxonMobil and Diamondback Energy

- 16 rigs currently active on the Acquired Assets

- Positions Freehold’s royalty lands to capture one in every three rigs active in the Midland Basin (almost doubling from one in every six rigs prior to the Acquisition)

“This acquisition is a successful reflection of our disciplined approach to strategic M&A, in an area we know well and further builds on the two core Midland Basin acquisitions we closed earlier this year. This fits precisely with our strategy of positioning our royalty portfolio in areas with best-in-class oil weighted reservoirs that have significant development runway under high quality operators. This transaction expands our footprint, right in the heart of the Midland Basin under ExxonMobil and Diamondback, two operators who recently completed a combined ~US$90 billion of acquisitions to increase their stakes in this extensive resource play” said David Spyker, Freehold’s President and Chief Executive Officer. “This type of accretive deal with land and inventory depth, provides both growth and value to the Company and our shareholders immediately and is expected to for years to come.”

Freehold will fund the Acquisition, which is expected to close December 13, 2024, through a $125.1 million bought deal equity financing (the Equity Financing) and Freehold’s existing credit facilities.

Acquisition Highlights

- Immediately adds significant production and a deep prospective multi-bench development inventory

- Freehold estimates 2025E production from the Acquired Assets to be 1,250 – 1,350 boe/d (approximately 61% light oil, 20% natural gas liquids and 19% natural gas) representing approximately $31 million in 2025E net royalty revenue (net of production and ad valorem taxes) based on US$70/bbl WTI, with limited tax burden in the near term

- Pro forma, almost doubles the share of drilling activity in the Midland Basin on Freehold’s royalty lands to one in every three wells drilled

- Adds 0.8 net drilled and uncompleted wells (DUCs) and permits, increasing Freehold’s line of sight total U.S. inventory by over 20% to 4.4 net activity wells

- More than 25% of the lands are characterized as undeveloped with no prior horizontal drilling activity. These lands are positioned to benefit from the most current drilling and frac stimulation methods as well as “cube development” that operators in the Midland Basin are prioritizing to maximize productivity and reserve recovery

- Increases Freehold’s exposure to premium priced, oil weighted production from the Midland Basin

- 61% oil weighting vs 51% on Freehold’s current total production base (Q1 – Q3 2024 average)

- 22% higher realized pricing from the Acquired Assets ($68.83/boe vs $56.34/boe Q1-Q3 2024 from Freehold’s current corporate asset base)

- Enhances Freehold’s alignment with investment grade operators with approximately 95% of current production from the Acquired Assets operated by ExxonMobil and Diamondback Energy

- ~244,000 gross drilling acres (including ~74,000 gross drilling acres that overlap with existing Freehold acreage) in the Midland Basin, increasing Freehold’s Midland Basin acreage by approximately 35%

- Approximately 85% of acreage is concentrated in the core of the Midland Basin in Martin and Midland counties, where over 50% of total drilling activity in the Midland Basin since 2022 has been concentrated

- Provides immediate and expected increasing future accretion on funds flow per share, free cash flow per share and total production and oil production per share

- Pro forma net debt to trailing 12 months funds from operations of 1.1x is below Freehold’s 1.5x leverage threshold

- Allows Freehold to continue to execute a consistent, sustainable return of capital program which balances dividend growth and accretive acquisition opportunities while maintaining a strong balance sheet

- Promptly following the closing of the Acquisition, Freehold is expecting that its senior credit facility will increase from $400 million to $450 million, maintaining its strong liquidity position post-Acquisition

- Freehold has an option to acquire up to an additional $65 million interest in the Acquired Assets, on the same terms and conditions, up until the closing of the Acquisition

Strategic Rationale

The Acquisition represents continued execution of our strategy to acquire mineral title and royalty interests in premier oil weighted basins across North America under best-in class operators. As Freehold has evolved over the last five years into a North American royalty company, the Midland Basin has become a core area for Freehold given the stacked-pay associated with multiple resource rich reservoir benches, robust drilling economics, and highly qualified, investment grade companies operating on our lands. The Midland Basin now comprises approximately 50% of Freehold’s pro forma U.S. production and ~20% of pro forma corporate production. ExxonMobil will be Freehold’s second largest corporate payor at approximately 13% of pro forma revenue, with ConocoPhillips at approximately 17% of pro forma revenue. Pro forma, Freehold’s revenue is balanced between Canada and the U.S. and our pro forma production is weighted approximately 59% in Canada and 41% in the U.S.

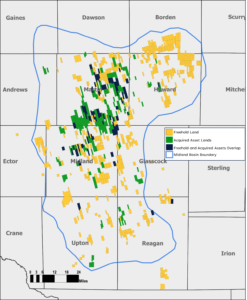

Figure 1: Acquired Assets Overview

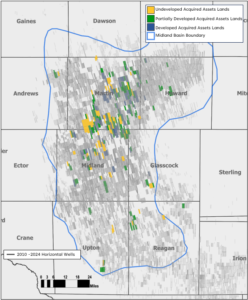

Figure 2: Acquired Assets – Stage of Development

Notes to Figure 2

Undeveloped Acquired Assets Land represents areas where there has been no horizontal well development to date on a drill spacing unit (DSU); Partially Developed means less than half of the expected total prospective development inventory on the DSU has been developed with horizontal wells; Developed means over half of the expected total prospective development inventory on the DSU has been developed with horizontal wells.

Acquisition Details

Promptly following the execution of the Acquisition purchase and sale agreement, Freehold has paid a deposit of approximately $11 million to be held in escrow until closing of the Acquisition. If the Acquisition does not close as a result of a breach of the Acquisition terms by the seller, Freehold is entitled to recover the deposit in addition to a break fee from the seller. The Acquisition terms also contain customary representations, warranties, covenants and conditions. Closing is expected to occur on December 13, 2024. Freehold has an option to acquire up to an additional $65 million interest in the Acquired Assets, on the same terms and conditions, up until the closing of the Acquisition. The effective date of the Acquisition is December 1, 2024.

In contemplation of the Acquisition, Freehold requested and received commitments from its syndicate of banks sufficient to increase its bank credit facilities by $50 million to $450 million with the accordion feature in such credit facilities conditional on closing of the Acquisition; however, Freehold does not require the additional available funds from the credit facilities increase to fund the purchase price of the Acquisition. The increase under the credit facilities will be subject to execution of definitive documentation by Freehold and its lenders consenting to such increase.

2025E Guidance Timing

Freehold plans to provide 2025E guidance estimates in connection with its year-end 2024 results on March 12, 2025 following the 2025 capital development plan announcements by Freehold’s strategic royalty payors.

Acquisition Financing

Freehold has entered into an agreement with a syndicate of underwriters co-led by RBC Capital Markets, CIBC Capital Markets and TD Securities Inc. (the Underwriters), pursuant to which the Underwriters have agreed to purchase for resale to the public, on a bought-deal basis, 9.62 million common shares (Common Shares) of Freehold at a price of $13.00 per Common Share for gross proceeds of approximately $125.1 million. The Underwriters will have an option to purchase up to an additional 15% of the Common Shares issued under the Equity Financing at a price of $13.00 per Common Share to cover over-allotments and for market stabilization purposes exercisable in whole or in part at any time until 30 days after closing of the Equity Financing.

Completion of the Equity Financing is subject to customary closing conditions, including the receipt of all necessary regulatory approvals, including the approval of the Toronto Stock Exchange. Closing of the Equity Financing is expected to occur on December 13, 2024. Closing of the Equity Financing is not conditional on the closing of the Acquisition. In the event that the Acquisition does not close, the net proceeds from the Equity Financing will be used to fund general corporate purposes including repayment of amounts outstanding under the Company’s credit facilities.

The Common Shares issued pursuant to the Equity Financing will be distributed by way of a prospectus supplement (the Prospectus Supplement) to the short form base shelf prospectus of the Company dated November 13, 2023 (together with the Prospectus Supplement, the Prospectus) and may also be offered and sold in the United States pursuant to an exemption from the registration requirements of the United States Securities Act of 1933, as amended (the U.S. Securities Act).

The Common Shares have not been and will not be registered under the U.S. Securities Act or any U.S. state securities laws, and may not be offered or sold in the United States or to, or for the account of benefit of, United States persons absent registration or any applicable exemption from the registration requirements of the U.S. Securities Act and applicable U.S. state securities laws. No securities regulatory authority has either approved or disapproved of the contents of this news release. This news release shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the securities in the United States or in any other jurisdiction in which such offer, solicitation or sale would be unlawful.

Access to the Prospectus, and any amendments to the documents are provided in accordance with securities legislation relating to procedures for providing access to a base shelf prospectus, a prospectus supplement and any amendment to the documents. The Prospectus will be (within two business days from the date hereof), accessible on SEDAR+ at www.sedarplus.ca.

An electronic or paper copy of the Prospectus (when filed), and any amendment to the documents may be obtained, without charge, from RBC Capital Markets by e-mail at Distribution.RBCDS@rbccm.com, from CIBC Capital Markets by e-mail at mailbox.canadianprospectus@cibc.com or from TD Securities Inc. by e-mail at sdcconfirms@td.com. The Prospectus will contain important detailed information about the Company and the proposed Offering. Prospective investors should read the Prospectus (when filed) and the other documents the Company has filed on SEDAR+ before making an investment decision.

Freehold is uniquely positioned as a leading North American energy royalty company with approximately 6.1 million gross acres in Canada and approximately 1.1 million gross drilling acres in the United States. Freehold’s common shares trade on the Toronto Stock Exchange in Canada under the symbol FRU.

| For further information, contact | |

| Freehold Royalties Ltd. | |

| Todd McBride, CPA, CMA | Nick Thomson, CFA |

| Investor Relations | Investor Relations |

| t. 403.221.0833 | t. 403.221.0874 |

| e. tmcbride@freeholdroyalties.com | e. nthomson@freeholdroyalties.com |

| w. www.freeholdroyalties.com | w. www.freeholdroyalties.com |

Forward-Looking Statements

This news release offers our assessment of Freehold’s future plans and operations as at December 9, 2024 and contains forward-looking information including, without limitation, forward-looking information with regards to the expected terms and conditions of the Acquisition; the expected timing for closing of the Acquisition; the expected attributes and benefits to be derived by Freehold pursuant to the Acquisition; the expected 2025 production from the Acquired Assets including the commodity weighting thereof; expected 2025 royalty revenue from the Acquired Assets; the expectation that there will be limited tax burden in the near term associated with the Acquired Assets; the expectation that Freehold’s royalty lands to capture one in every three rigs active in the Midland Basin; the expectation that the Acquired Assets have a significant development runway under high quality operators; the net DUCs and permits associated with the Acquired Assets; the expectation that more than 25% of the lands associated with the Acquired Assets are characterized as undeveloped with no prior horizontal drilling activity; the expectation that lands associated with the Acquired Assets are positioned to benefit from the most current drilling and frac stimulation methods as well as “cube development” that operators in the Midland Basin are prioritizing to maximize productivity and reserve recovery; the expectation that the Acquisition will increase Freehold’s exposure to premium priced, oil weighted production from the Midland Basin; the expectation that together with the Equity Financing, Freehold estimates that the Acquisition provides immediate and increasing future accretion on funds flow per share, free cash flow per share and total production and oil production per share; the expectation that the Acquisition together with the Equity Financing will allow Freehold to continue to execute a consistent, sustainable return of capital program which balances dividend growth and accretive acquisition opportunities while maintaining a strong balance sheet; Freehold’s forecast pro forma net debt to trailing 12 months funds from operations of 1.1x being below Freehold’s 1.5x leverage threshold after giving effect to the Acquisition and the Equity Financing; Freehold’s plan to provide 2025E guidance estimates in connection with its year-end 2024 results on March 12, 2025 following the 2025 capital development plan announcements by Freehold’s strategic royalty payors; the expected terms of the Equity Financing; the expected use of proceeds from the Equity Financing; the expected timing of closing the Equity Financing; and the expected increase to Freehold’s credit facilities which is expected to provide Freehold with a strong liquidity position.

This forward-looking information is provided to allow readers to better understand our business and prospects and may not be suitable for other purposes. By its nature, forward-looking information is subject to numerous risks and uncertainties, some of which are beyond our control, including the demand for oil and natural gas, general economic conditions, industry conditions, the impact of the Russia-Ukraine war and the Israel-Hamas-Hezbollah conflict on the global economy and commodity prices, volatility of commodity prices, currency fluctuations, imprecision of reserve estimates, royalties, environmental risks, taxation, regulation, changes in tax or other legislation, competition from other industry participants, the lack of availability of qualified personnel or management, stock market volatility, our ability to access sufficient capital from internal and external sources. The closing of the Acquisition, and/or Equity Financing could be delayed if Freehold or the other parties are not able to obtain the necessary regulatory and stock exchange approvals on the timelines anticipated. The Acquisition and/or Equity Financing may not be completed if these approvals are not obtained. The closing of the Acquisition may not be completed if some other condition to the closing of the Acquisition is not satisfied. Accordingly, there is a risk that the Acquisition, Equity Financing will not be completed within the anticipated time or at all. In addition, the Equity Financing is not conditional on the closing of the Acquisition and as such the proceeds from the Equity Financing may be used for purposes other than the payment of the purchase price pursuant to the Acquisition. Risks are described in more detail in Freehold’s annual information form for the year ended December 31, 2023 which is available under Freehold’s profile on SEDAR+ at www.sedarplus.ca.

With respect to forward looking information contained in this press release including relating to the 2025 forecast production and 2025 royalty revenue from the Acquired Assets, we have made assumptions regarding, among other things; future oil and natural gas prices (for the purposes of the estimates in this press release we have assumed a West Texas Intermediate price of US$70/barrel of oil and a NYMEX natural gas price of US$3.30/MMbtu); future exchange rates (for the purposes of the estimates in this press release we have assumed an exchange rate of US$1.00 for every CDN$1.40); that drilled uncompleted wells will be completed in the short term and brought on production; that wells that have been permitted will be drilled and completed within a customary timeframe; expectations as to additional wells to be permitted, drilled, completed and brought on production in 2024 and 2025 based on Freehold’s review of the geology and economics of the plays associated with the Acquired Assets; expected production performance of wells to be drilled and/or brought on production in 2024 and 2025; the ability of our royalty payors to obtain equipment in a timely manner to carry out development activities; the ability and willingness of royalty payors to fund development activities relating to the Acquired Assets; and such other assumptions as are identified herein. You are cautioned that the assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be imprecise and, as such, undue reliance should not be placed on forward looking information. We can give no assurance that any of the events anticipated will transpire or occur, or if any of them do, what benefits we will derive from them. The forward-looking information contained herein is expressly qualified by this cautionary statement. To the extent any guidance or forward-looking statements herein constitute a financial outlook, they are included herein to provide readers with an understanding of management’s plans and assumptions for budgeting purposes and readers are cautioned that the information may not be appropriate for other purposes. Our policy for updating forward-looking statements is to update our key operating assumptions quarterly and, except as required by law, we do not undertake to update any other forward-looking statements. You are further cautioned that the preparation of financial statements in accordance with International Financial Reporting Standards requires management to make certain judgments and estimates that affect the reported amounts of assets, liabilities, revenues, and expenses. These estimates may change, having either a positive or negative effect on net income, as further information becomes available and as the economic environment changes.

Currency

All references in this press release to dollar amounts are to Canadian dollars unless otherwise indicated.

Conversion of Natural Gas to Barrels of Oil Equivalent (BOE)

To provide a single unit of production for analytical purposes, natural gas production and reserves volumes are converted mathematically to equivalent barrels of oil (boe). We use the industry-accepted standard conversion of six thousand cubic feet of natural gas to one barrel of oil (6 Mcf = 1 bbl). The 6:1 boe ratio is based on an energy equivalency conversion method primarily applicable at the burner tip. It does not represent a value equivalency at the wellhead and is not based on either energy content or current prices. While the boe ratio is useful for comparative measures and observing trends, it does not accurately reflect individual product values and might be misleading, particularly if used in isolation. As well, given that the value ratio, based on the current price of crude oil to natural gas, is significantly different from the 6:1 energy equivalency ratio, using a 6:1 conversion ratio may be misleading as an indication of value.